The state and the green economy

As the objectives of the Paris Agreement on climate change make clear, greenhouse gas emissions need to decline substantially by 2050 to prevent disastrous global warming. Existing commitments at country level — both in the EBRD regions and elsewhere — are not strong enough to achieve that goal. The scale and urgency of what is needed over the next 30 years is such that an assertive state is required to guide private initiative. In the short term, the transition to a green economy should be built into Covid-19 recovery packages. In the medium term, the state needs to address the barriers, market imperfections and policy failures which are impeding that transition. And in the longer term, the state must support the “creative destruction” which that transition process will unleash, while at the same time making sure that it is equitable and smooth.

Introduction

Global warming is widely recognised as posing a major threat to humanity. Recent changes in weather patterns, rising sea levels and more frequent extreme weather events have caused widespread economic damage and loss of human life. The Intergovernmental Panel on Climate Change (IPCC) has warned that we have only a few years left to radically decarbonise the world economy if disastrous global warming is to be avoided.1

Climate change and other environmental problems do not observe national borders and can only be managed through timely collective action. The 2015 Paris Agreement on climate change2 provides an opportunity for countries to strengthen the global response to climate change by keeping global temperature rises well below 2°C – and ideally as low as 1.5°C – relative to pre-industrial levels.

The scale and urgency of what is required over the next 30 years will pose unprecedented challenges for the state. It will require the state to play a more central role, guiding, enforcing and coordinating the transition to a green economy. This is not a case of “Central Planning 2.0”; it is about steering private initiative in the right direction. The Covid-19 pandemic has shown just how vulnerable the global economic system can be in the face of system-wide risks, so the need to transition to a green economy remains urgent even as governments prioritise public health and battle the economic fallout from the pandemic.

This chapter looks at the role of the state in the transition to a green economy. It begins by assessing the ambitions of economies in the EBRD regions in terms of achieving the goals of the Paris Agreement and supporting the transition to a green economy. It describes actions taken at state level in the form of policies and laws and examines their impact on greenhouse gas (GHG) emissions. It also provides guidance on the state’s role in that transition process in the short, medium and longer term, drawing on existing evidence. Lastly, this chapter concludes by looking at the role of the private sector in the transition to a green economy.

Taking stock

Climate change objectives under the Paris Agreement

This chapter starts by looking at climate change objectives set at state level in various economies. The adoption of the Paris Agreement at the United Nations Climate Change Conference of the Parties in 2015 (COP 21) was one of the biggest climate change milestones in history. The overarching aim of the Paris Agreement is to reduce GHG emissions and ensure that global temperature increases this century remain well below 2°C relative to pre-industrial levels, while ideally pursuing a scenario whereby temperature rises remain below 1.5°C.

As of September 2020, a total of 197 parties have signed the agreement, and 189 of them have ratified it. All of the economies in the EBRD regions have signed and ratified the Paris Agreement, with the exception of Turkey (which has signed it, but not yet ratified it) and Kosovo (which is not a member of the UN). Under the agreement, all parties are required to set out the contributions that they intend to make to the objectives of the Paris Agreement in a formal submission to the UN. Those “nationally determined contributions” (NDCs) include all efforts to reduce national emissions and adapt to the impact of the changing climate.

All of the economies in the EBRD regions have taken some action on climate change and managed to reduce their GHG emissions relative to the levels seen in the early 1990s.3 However, the reductions and ambitions seen to date fall short of what is required to achieve the objectives of the Paris Agreement. Comparing NDCs across economies is difficult, because they vary in terms of their mitigation targets and the years by which those objectives are to be achieved, as well as using differing methodologies and measuring targets against different base years. In the EBRD regions, 22 economies have an absolute GHG emission reduction target, 11 have a “business as usual” (BAU) target (whereby no additional emission reduction policies are adopted between the submission of the NDC and the target year), two economies have a target of reducing the carbon-intensity of GDP, and another two economies only list policies and actions. The most common base years are 1990 and 2005, but 2000, 2010, 2013 and 2030 are also used. All but two economies have chosen 2030 as their target year.

However, standardising those methodologies and combining them with various assumptions on GDP growth and UN projections on population growth makes such a comparison possible.4 The analysis in this chapter focuses on the economies of the EBRD regions and a limited number of comparator countries: China, the United Kingdom, the United States of America and EU member states outside the EBRD regions.

Most economies are committed to reducing GHG emissions relative to GDP (see Chart 4.1). Indeed, GHG emissions per unit of GDP are expected to fall by 2030 in all but five economies in the EBRD regions, with reductions potentially ranging from as little as 3 per cent in Morocco to 63 per cent in the Kyrgyz Republic. At the same time, NDC commitments in Turkey imply a 5 per cent increase in emissions per unit of GDP, and commitments in Lebanon involve emissions potentially more than doubling relative to GDP. In comparator economies, meanwhile, GHG emissions per unit of GDP are expected to decline by between 42 and 52 per cent.

The planned reduction in GHG emissions per unit of GDP is not enough to offset the pollution that is associated with expected GDP growth. Indeed, in most of the economies in the EBRD regions, those targets imply a rise in emissions between 2010 and 2030 – with emissions increasing by more than 150 per cent in some instances (as in the case of Tajikistan, Turkmenistan, Uzbekistan, and the West Bank and Gaza, for instance; see Chart 4.2). There are only 13 economies where NDCs imply reductions in GHG emissions between 2010 and 2030, with those reductions ranging from 0.5 per cent in Lithuania to 25 per cent in Cyprus.

In 2016, a number of economies (including Armenia, Belarus, Bulgaria, Croatia, Greece, Hungary, Kazakhstan, Lithuania, Moldova, Montenegro, North Macedonia, Romania, Serbia, the Slovak Republic, Slovenia and Ukraine) had absolute emissions that were below the 2030 target set out in their NDCs. This is not surprising, given that GHG emissions in most of those countries were much higher in their chosen base year (1990 or 2005 in most cases) than they were in 2010 or 2016, owing to the cheap energy and chronic environmental neglect of the central planning era.5 However, it does highlight the fairly unambitious nature of the emission reduction targets in NDCs, particularly as regards absolute reductions in GHG emissions.

At an aggregate level, NDC commitments imply a decline in the absolute emissions of advanced economies (as defined by the IMF) and an increase in the absolute emissions of emerging market and developing economies (see Chart 4.3). This pattern is consistent with the principle of “common but differentiated responsibilities and respective capabilities”, under which advanced economies – which are responsible for most of the GHGs in the atmosphere and have greater scope to act – are expected to take the lead in the fight against climate change by reducing their own GHG emissions, as well as providing support to developing economies.

Despite that principle, deeper and faster cuts in emissions will be required in the future, and countries will need to indicate those reductions in the second round of NDCs, starting in 2020. Globally, GHG emissions have been rising at a rate of 1.5 per cent per year over the last decade, without any sign of peaking. In the second round of NDCs, countries will need to strengthen their NDC ambitions threefold in order to achieve the 2°C goal and more than fivefold in order to achieve the 1.5°C goal.6

Support for the transition to a green economy

The climate change ambitions of individual governments reflect the opinions of the voters and stakeholders that those governments represent. In the EBRD regions, many economies continue to specialise in energy intensive industries – a legacy of the central planning era. Analysis of international trade statistics in the UN Comtrade database shows that highly energy-intensive industries7 account for more than 50 per cent of total goods exports in Azerbaijan, Belarus, Egypt, Greece, Kazakhstan, the Kyrgyz Republic, Montenegro, Russia, Tajikistan and Uzbekistan.

Moreover, consumers have become accustomed to cheap – often subsidised – energy. Consequently, the politics of decarbonisation reforms has been extremely challenging. In the Kyrgyz Republic, for example, the government approved increases in residential tariffs in 2009, accompanied by subsidies for low income households through state-run social assistance programmes, but political unrest led to a reversal of that increase and a change in government in 2010.8

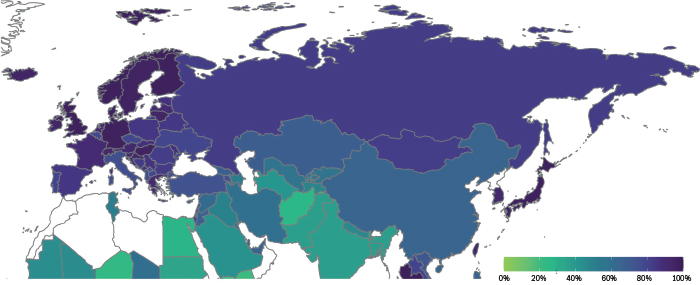

Thus, the transition to a green economy requires determined political leadership, as well as good public policy and strong state institutions. However, it also offers the prospect of healthier, safer, cleaner and more sustainable forms of economic prosperity. Increasingly, political leaders have the support of their citizens in this regard – not least among the young, whose futures may be directly affected by any failings in this area. Overall, people living in the EBRD regions claim to have a reasonably good understanding of climate change, on the basis of the results of representative household surveys (see Chart 4.4). However, while the percentage of people who claim to know at least something about climate change stands at more than 90 per cent in central Europe and the Baltic states (CEB), it remains below 60 per cent in the southern and eastern Mediterranean (SEMED) region and Central Asia.

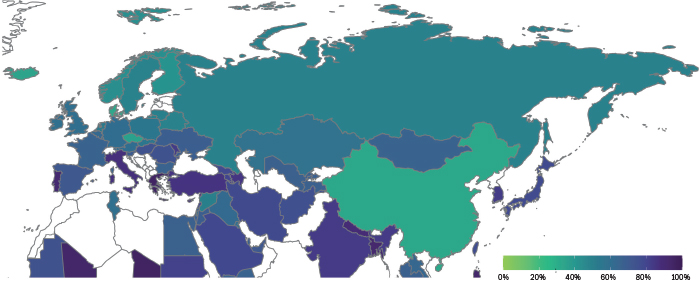

In the EBRD regions, the percentage of respondents who see global warming as a personal threat is highest in Greece (96 per cent) – which is not surprising, given that people living on its many islands can see the threat much more clearly than the inhabitants of, say, land-locked Belarus (49 per cent; see Chart 4.5). Overall, people living in less developed economies tend to regard climate change as a greater personal threat than people in developed economies (see Chart 4.5).

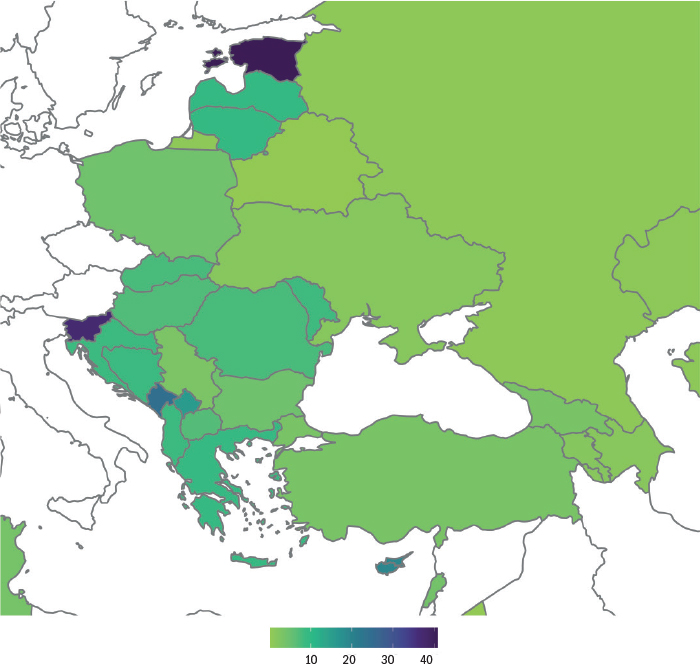

However, the perception that climate change is a threat does not necessarily translate into action, as highlighted by recent data on the Fridays for Future (FFF) movement – an international initiative whereby schoolchildren, inspired by Greta Thunberg, take time off from school on Fridays to participate in demonstrations, demanding action from political leaders to prevent climate change and calling for the fossil fuel industry to transition to renewable energy. Measured in per capita terms, demand for action on climate change is particularly strong in Estonia, Slovenia and Montenegro (see Chart 4.6), with the number of climate strikes per capita between November 2018 and May 2020 exceeding equivalent figures for the United Kingdom and the United States of America, as well as the EU average. In the EBRD regions, climate strikes tend to be less common than in advanced economies but slightly more common than in other emerging market economies. For details of the impact that the Covid-19 crisis has had on people’s concerns about climate change, see Box 4.1.

Action in the form of laws and policies

Another way of assessing the performance of economies is to look at the green policies and measures that have been implemented and their effect. All economies in the EBRD regions have adopted laws and policies tackling climate change. Analysis of a dataset combining the IEA Policies and Measures Database and the Climate Change Laws of the World database with additional research on green laws and policies in Kosovo, North Macedonia and the West Bank and Gaza reveals that, by 2019, economies in the EBRD regions had adopted a total of 248 green laws (parliamentary acts or government edicts) and 560 green policies (principles, rules and guidelines) at national level (with EU member states being subject to a further 57 laws and 68 policies adopted at European level; see Annex 4.2). As Chart 4.7 shows, the number of green laws and policies being adopted has increased dramatically since the 1990s, both in the EBRD regions and elsewhere. The majority of those laws and policies are regulatory in nature (introducing environmental standards, for instance). Information and agreement-based policies were popular early on, with policies involving taxes and levies gaining in traction over time.

The regression analysis presented in Table 4.1 (column 1) indicates that passing a green law or adopting a green policy is associated with declining CO2 emissions per unit of GDP, over both the short and the long term.9 That analysis links GHG emissions per unit of GDP to the introduction of green laws and policies, taking account of various country-level characteristics, as well as country and year fixed effects.

What ultimately matters, however, is the enforcement of such green laws and policies in order to achieve effective reductions in emissions. The regression analysis also shows that the magnitude of the impact depends on the strength of enforcement (captured here by the Worldwide Governance Indicator measuring the rule of law). In a country with the strongest recorded score for the rule of law, passing a new green law is associated with a 0.7 per cent per unit of GDP reduction in annual CO2 emissions in the short term and 1 per cent in the long term. In contrast, adopting a new green policy in a country with the weakest recorded score for the rule of law is associated with only 0.2 per cent per unit of GDP emissions reduction in the long term. Given the governance gap between the economies of the EBRD regions and advanced economies, which has been well documented,10 a climate law or policy that is adopted in the EBRD regions can be expected to have a weaker impact on emissions than an equivalent law or policy adopted in an advanced economy.

Green laws and policies are associated with reduced CO2 emissions from the EBRD regions totalling 12 per cent between 1997 and 2016 relative to the levels that would otherwise have been seen (see Chart 4.8). This is an encouraging start, but much more will need to be done to accelerate the transition to a green economy. The sections that follow assess the various short, medium and long-term options in terms of possible government interventions.

Chart 4.1

- 2010 level – carbon intensity of GDP target

- 2010 level – other target

- 2030 estimate/range

Source: NDC Registry, EU (2018), Climate Analysis Indicators Tool (CAIT), GDP growth forecasts (produced by the EBRD, the IMF and the OECD) and authors’ calculations.

Note: See Annex 4.1 for details. Kosovo is not a member of the UN, so has not submitted an NDC. The West Bank and Gaza have non-member observer status at the UN. Egypt’s NDC does not set a specific target. GDP estimates for 2030 are not available for the West Bank and Gaza. Economies are ordered on the basis of the GHG emissions per unit of GDP in 2030 that are implied by their NDC targets, from the highest to the lowest. Economies with red bars have targets aimed at reducing the carbon intensity of GDP by 2030, while those with blue bars have other types of target. Turkmenistan’s NDC does not set a target as such, but mentions a desire to achieve a specific reduction in emission levels per unit of GDP.

Chart 4.2

- 2010 level – absolute target

- 2010 level – other target

- 2030 estimate/range

Source: NDC Registry, EU (2018), CAIT, GDP growth forecasts (produced by the EBRD, the IMF and the OECD) and authors’ calculations.

Note: See the note accompanying Chart 4.1.

Chart 4.3

- 2010 level

- 2030 estimate/range

Source: NDC Registry, EU (2018), CAIT, GDP growth forecasts (produced by the EBRD, the IMF and the OECD) and authors’ calculations.

Note: See the note accompanying Chart 4.1. This chart is based on data for 138 economies. Seven of the economies in the EBRD regions are classified as “advanced economies”: Cyprus, Estonia, Greece, Latvia, Lithuania, the Slovak Republic and Slovenia.

Chart 4.4

People living in the EBRD regions claim to have a reasonably good understanding of climate change

Source: Gallup Poll 2008-10 and authors’ calculations.

Note: This map shows the percentage of survey respondents who claim to know “a great deal” or “something” about global warming or climate change. No data are available for the economies in white. This map is used for data visualisation purposes only and does not imply any position on the legal status of any territory.

Chart 4.5

Inhabitants of less developed economies tend to regard climate change as a greater personal threat

Source: Gallup Poll 2008-10 and authors’ calculations.

Note: This map shows the percentage of survey respondents who feel that global warming is either a “very serious threat” or a “somewhat serious threat” to them and their family. No data are available for the economies in white. This map is used for data visualisation purposes only and does not imply any position on the legal status of any territory.

Chart 4.6

In Estonia, Slovenia and Montenegro, the number of school strikes per capita is higher than the average for the EU-27

Source: Fridays for Future, World Development Indicators and authors’ calculations.

Note: This map shows the number of school strikes per million of population in the period from November 2018 to May 2020. This map is used for data visualisation purposes only and does not imply any position on the legal status of any territory.

Chart 4.7

Source: IEA Policies and Measures Database, Climate Change Laws of the World database, and authors’ research and calculations.

Chart 4.8

Source: Authors’ calculations.

Note: These data are based on the estimates presented in columns 1 and 2 of Table 4.1.

The role of the state in the short term

In the short term, policies supporting the transition to a green economy need to be coordinated with efforts to support the economic recovery following the Covid-19 crisis. The objectives of the transition to a green economy and the post-Covid-19 recovery are not necessarily in conflict with one another. Indeed, sustainability concerns should be built into any recovery package. Stimulus measures have to be timely (that is to say, shovel-ready), focus on investment that generates local jobs in the short run, and aligned with long-term national and global objectives in the area of sustainable development. In other words, the stimulus needs to foster transition to a green economy and focus on zero-carbon investment with a significant multiplier effect. In order to meet the 2°C target set by the Paris Agreement, all investment should, from now on, be consistent with achieving net-zero emissions by 2050 (meaning that a balance is struck between releasing emissions into the atmosphere and removing them by means of carbon sinks such as forests).11

Such measures can involve improvements in infrastructure (in the transport, communication, energy and water sectors, for instance), investment in renewable energy, spending on general R&D or research in the area of clean energy, extensive retrofitting of government-owned buildings, investment in energy-efficient residential buildings or the use of energy management systems.12 Measures such as investment in connectivity infrastructure and investment in renewable energy generate more employment in the short term,13 when jobs are scarce amid the recession. In the long term, these investments then require less labour for operations and maintenance, thus freeing up labour as the economy returns to pre-Covid-19 capacity. In addition, renewables also save on fuel and are better for the environment.

Supporting homeowners who want to improve the energy efficiency of their homes has a similar effect: it creates jobs, and it comes with environmental, economic and social benefits. It reduces buildings’ emissions, lowers energy bills and creates a comfortable environment for residents. In the EBRD regions, for instance, the Bank has helped around 120,000 households to invest in high-quality green technologies such as thermal insulation, lighting, windows and doors, domestic appliances, heat pumps and solar panels through dedicated credit lines, in partnership with 40 financial institutions across 12 economies, helping to prevent 356,000 tonnes of CO2 emissions per year.14

More broadly, it is important to recover from the pandemic in a way that makes businesses resilient to future shocks. This includes preparing them for the transition to a green economy. Rather than propping up zombie firms that have little chance of surviving in the green economy, the state can design its support packages in a way that readies businesses for the future.

For example, the labour productivity of manufacturing firms varies widely across the EBRD regions, but firms vary even more when it comes to electricity consumption per unit of output. This is true even when looking at differences within relatively narrowly defined industries (see Chart 4.9). This means that many firms are not operating anywhere near the energy efficiency frontier. Consider, for example, an industry in central Europe and the Baltic states with average dispersion of electricity consumption per unit of output. In that industry, an establishment in the 90th percentile of electricity efficiency produces more than 68 times the output of an establishment in the 10th percentile while using the same amount of electricity. Such differentials tend to be even larger in other EBRD regions. In part, they reflect differences in electricity costs (inclusive of any subsidies). However, they also point to the inefficient use of energy.

This, in turn, suggests that there is potential to improve energy performance. Covid-19 support should therefore be used to help firms reach the energy efficiency frontier. Such a support package could include free energy audits for firms, which could highlight the physical and behavioural changes that are needed to reduce energy consumption. In exchange for receiving free energy audits, firms could, as a minimum, be required to implement the low-cost operational or maintenance adjustments that are recommended in order to save energy (for example, switching equipment on and off as required, rather than at the start and end of each shift). Where an audit identifies a need for investment in energy efficiency measures, the firm could be given access to subsidised financing, perhaps in return for adopting energy efficiency performance targets. In addition to reducing firms’ energy bills, such measures will also contribute to economy-wide efforts to achieve targets set under the Paris Agreement.

Chart 4.9

- Interquartile range

- Average

Source: Enterprise Surveys and authors’ calculations.

Note: These observations show, for each measure of productivity listed on the y-axis, the difference in terms of the logarithm of productivity between firms in the 90th and 10th percentiles of the productivity distribution for 170 manufacturing industries across the EBRD regions and the Czech Republic, taking into account industry fixed effects. The median for each measure is indicated by a vertical line. Extreme values (1.5 times the interquartile range above the third quartile or below the first quartile) are denoted by the ends of the horizontal lines.

Chart 4.10

Source: Coady et al. (2019) and authors’ calculations.

The role of the state in the medium term

In the medium term, the state needs to address the barriers, market imperfections (externalities) and policy failures that are impeding the transition to a green economy. Many of these actions will also have wider economic and environmental benefits, such as better functioning markets and a cleaner environment.

The first step is to get prices right. Energy prices need to reflect the economic and environmental costs of the relevant fuel type. This means that a cost should be applied to carbon pollution in order to encourage polluters to reduce their emissions (in contrast with the existing energy subsidies, which effectively incentivise firms to pollute more).

Fossil fuel subsidies

In the EBRD regions, more than 70 per cent of GHG emissions originate in the energy sector, with fossil fuels (which include coal, oil and gas) being used to generate 81 per cent of all electricity in those regions in 2015.15 Moreover, in several countries in the EBRD regions that are heavily reliant on fossil fuels for their energy supply, subsidies are applied to both fossil fuels and electricity generated from fossil fuels. By reducing the cost of driving diesel and petrol cars or burning fossil fuels for heating and electricity, such subsidies attach a negative price to carbon emissions. That encourages pollution and incentivises inefficient use of carbon-intensive energy.16

IMF estimates suggest that pre-tax subsidies on fossil fuels (where the cost of supplying fuels exceeds their domestic price) declined between 2010 and 2017 in the EBRD regions, both in absolute terms and relative to GDP (see Chart 4.10).17In Uzbekistan, for instance, pre-tax subsidies fell from more than 25 per cent of GDP in 2010 to 8 per cent in 2017, and they fell from 21 per cent to 8 per cent over the same period in Turkmenistan. They also declined as a percentage of GDP in Egypt, Morocco, Russia and Ukraine, but they increased in Albania, Armenia, Azerbaijan, Belarus, Jordan, Kazakhstan, the Kyrgyz Republic, Lebanon, Mongolia, Tajikistan and Tunisia.

Carbon pricing

Putting a price on carbon is arguably the most important step in terms of addressing climate change, although it is not sufficient on its own. Carbon pricing will begin to correct the fundamental externality that lies at the heart of this problem, making emitters of GHGs confront the environmental costs of their actions.

The EBRD regions are home to a number of early adopters of carbon pricing, such as Poland (1990), Slovenia (1996), Estonia (2000) and Latvia (2004). Carbon pricing was given a major boost in 2005 with the establishment of the EU Emissions Trading System (ETS), which all of the EU member states in the EBRD regions participate in. Outside of the EU, Ukraine implemented carbon pricing in 2011 and Kazakhstan followed suit in 2013.18

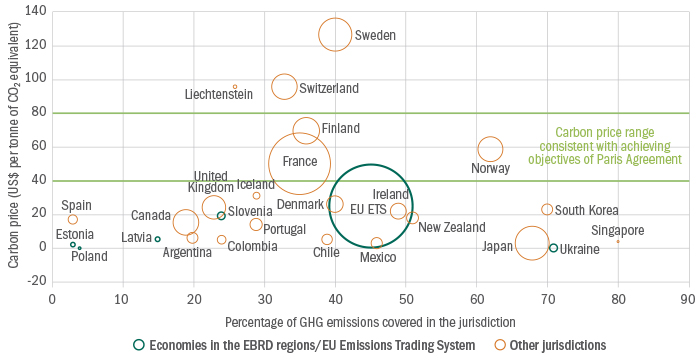

The effectiveness of a carbon-pricing scheme depends on two factors: its scope (that is to say, the percentage of total emissions covered), and the price. While the percentage of emissions covered is relatively high in some countries (such as Ukraine), only 20 per cent of the world’s emissions are covered by a carbon price. Moreover, the price of carbon is too low overall (see Chart 4.11).

In 2017, the High-Level Commission on Carbon Prices estimated that carbon prices would need to rise to between US$ 40 and US$ 80 per tonne of CO2 by 2020 in order to deliver on the Paris Agreement.19 Even the EU ETS prices carbon below that level; and in Poland, Estonia, Latvia and Ukraine, the price is only just above zero.

Some argue that carbon pricing could be detrimental to the competitiveness of highly energy intensive industries, even though there is little empirical evidence to support that claim.20 In order to address such concerns, policymakers in many countries have been considering “carbon border adjustments” – import tariffs proportionate to the carbon content of goods imported from countries without adequate carbon pricing – in order to guard against “emissions leakage”. The European Commission launched a public consultation on energy taxation and a carbon border adjustment mechanism in July 2020. While the precise details (including the sectors that will be subject to that measure) have yet to be determined, goods produced in highly energy-intensive industries are more likely to be affected. In several non-EU economies in the EBRD regions, highly energy-intensive industries accounted for more than 10 per cent of total goods exported to the EU in the period 2015-18. And in the case of North Macedonia and Russia, that figure stood at more than 30 per cent (see Chart 4.12). Having their own carbon taxes would exempt countries from the carbon border adjustment tax and enable them to keep the revenues in their own countries, as well as providing an incentive for firms to invest in improving energy efficiency.

Carbon pricing has a low implementation cost and is highly efficient, encouraging low-carbon adjustments all along the supply chain through producers’ decisions on intermediate inputs and consumers’ choices on final goods. Individual emitters facing a carbon price are probably better placed to identify the best way to reduce their carbon output than regulators, who may otherwise opt for more stringent industry standards.

However, carbon pricing can be regressive. Most carbon tax is paid on energy (heating and electricity), which accounts for a larger percentage of the expenditure of lower-income households. Protests in the Kyrgyz Republic in 2010 attest to consumers’ potential sensitivity to changes in energy prices. Indeed, public opposition is one of the main obstacles to the implementation of carbon taxes. Experience to date suggests that carbon taxes should be phased in gradually, with their proceeds being earmarked for additional climate change mitigation measures, as well as support for lower-income households.

In particular, the adverse distributional effects of carbon pricing could be addressed by means of transfers to lower-income households (funded by additional revenue raised through carbon pricing), coupled with targeted subsidies encouraging improvements to residential energy efficiency. Policymakers should ensure that they keep the public informed about carbon-pricing initiatives at all stages of the process, from the design stage right through to implementation.21

Nevertheless, carbon prices alone are not sufficient to trigger structural change on the necessary scale within the necessary timescale.22 Many structural challenges, such as the design of cities and production networks, respond slowly or weakly to changes in prices, owing to inertia in business decisions, information barriers (see below) and other rigidities.

Other barriers impeding the transition to a zero-carbon economy

In addition to the failure to “internalise” environmental externalities, there are also various other factors that are impeding the transition to a zero-carbon economy. Clean energy represents a public good, meaning that the social benefits of R&D in this area may far exceed private benefits on account of largely un-monetised benefits such as better air quality and healthier lifestyles. This results in an insufficient supply of green innovation. Failures in capital markets may also limit the amount of green financing available. Moreover, green innovation also relies on network effects and is thus vulnerable to coordination failures – as can be seen, for example, when it comes to establishing carbon capture and storage (CCS) clusters or providing the infrastructure needed to charge electric vehicles.

As a result, energy efficiency levels fall short of the potential level (giving rise to what is termed the “energy efficiency gap”). Some of this gap can be explained by hidden costs, such as the cost of obtaining relevant information about energy-efficient technologies and the risks associated with their deployment. The opportunity cost of alternative investments that are forgone in order to invest in energy efficiency (including the cost of scarce managerial attention), which are not included in engineering estimates, also plays a role.23 However, a large percentage of the energy efficiency gap reflects under-pricing of energy and uncertainty about future energy prices.24

Information barriers appear to play an important role in the EBRD regions. More than 60 per cent of firms that have not invested in energy efficiency improvements say that their main reason for not doing so is that they do not see them as a priority, with only 12 per cent blaming a lack of funding for green investment.25 This could reflect imperfect information (or a lack of information) about the savings that can be made as a result of investing in more energy-efficient machinery or equipment, making companies disinclined to invest in them. In comparison, only 12.5 per cent of surveyed firms say (rightly or wrongly) that energy efficiency investments are unprofitable. Box 4.2 looks at how an online platform can be used to improve the dissemination of information about green technologies and associated funding options.

A lack of financial resources is the third most cited reason for not investing in energy efficiency. In the absence of a regulatory nudge, investors find it difficult to embrace projects that involve new, climate friendly solutions. The perception of a high degree of risk is driven by the significant upfront costs associated with certain technologies, as well as the untested nature of new business models lacking historical performance data. However, awareness of green issues in the financial markets is gradually increasing (see Box 4.3).

Chart 4.11

The overall carbon price remains below the price range that would be consistent with achieving the objectives of the Paris Agreement

Source: World Bank (2019), High-Level Commission on Carbon Prices (2017) and authors’ calculations.

Note: The size of each circle denotes the nominal amount of government revenue that is generated by carbon pricing.

Chart 4.12

Source: UN Comtrade, Kosovo Statistical Agency and authors’ calculations.

Note: Highly energy-intensive industries are defined on the basis of Upadhyaya (2010). Data for Kosovo relate to the period 2016-18.

The role of the state in the long term

The economic changes that are required in order to transition to a green economy are deep, structural and systemic. Indeed, they are sometimes considered to be akin to a new industrial revolution.26 The state has an important role to play in this process of creative destruction. A proactive role for the state does not mean a move towards widespread state ownership or government-directed economic activity. It means strengthening public policy in order to address the market failures discussed in the previous section and integrate environmental policies into a wider industrial strategy aimed at achieving clean growth. And as creative destruction inevitably creates both winners and losers, public policy also needs to mitigate the risks for those who are adversely affected by the transition to a green economy.

A green industrial policy needs to anticipate long-term technological trends and promote broader structural change across the economy – not just in industrial sectors. This kind of shift to a low-carbon economy can also deliver resource efficiency and productivity enhancements, thereby improving the competitiveness of the economy as a whole.

Traditional industrial policies and green industrial policies are similar in many ways. Both steer the economy towards an increase in value added and enhanced productivity. Both entail risks relating to political capture and the misallocation of scarce resources. And the trade-offs that are inherent in traditional industrial policy also apply to green industrial policy, as do the lessons that have been learned regarding politically connected firms and the governance of state-owned enterprises (see Box 1.8 and Chapter 2).

Support for clean innovation

The transition to a green economy relies on technological change: a switch from polluting to clean technologies (from traditional internal combustion engines to electric and hybrid vehicles, for example). However, innovation tends to exhibit a high degree of path dependence. Firms that have historically carried out a lot of innovation in relation to dirty technologies will find it easier to continue innovating in those areas. At the same time, a firm is more likely to innovate in areas relating to clean technologies if it is located in a country where other firms have been innovating in such areas.27 In addition, the types of technology that are developed will be influenced by the relative prices of energy inputs.28

This indicates that the state has a role to play in supporting technological change. Carbon pricing is key in this regard, but on its own it may not necessarily result in firms switching to clean innovation given the extent of technological path dependence. The state needs to encourage the development of clean technologies of the future by subsidising R&D in such areas.29 Increased state support for radical new clean technologies is also justified by the substantial knowledge spillovers that they produce, which are comparable to those seen in nanotechnology or information technology (IT).30 Since knowledge developed by one firm can often be used by competitors for a fraction of the cost of developing it, firms may otherwise invest too little in knowledge development relative to the level that would be optimal for society as a whole.

In order to assess trends in clean innovation in the EBRD regions, this chapter now turns its attention to the subject of clean patents. Although innovation rates tend to be low in many economies in the EBRD regions, clean patents account for a relatively large percentage of total patents in those regions (averaging around 9.6 per cent of total patents, compared with an average of 6.4 per cent in advanced economies; see Chart 4.13). In fact, prior to 2004, clean patents’ share of total patents was actually higher in the EBRD regions than it was in the rest of the world, albeit the overall patenting rate in the EBRD regions was far lower.

In countries that primarily adopt – rather than develop – new technologies (including many economies in the EBRD regions), governments could foster the diffusion of technology by making it easier for firms to participate in global value chains and hire individuals with the requisite skills. In contrast, local content policies (which are a common component of industrial policy in areas such as renewable energy) may slow technological change down instead of deepening it (see Box 4.4).

Support for technological change needs to be immediate and decisive, but it does not need to be permanent. Once more firms have started engaging in clean innovation and using clean technologies, the rest will follow, thanks to knowledge spillovers and network effects. For instance, when the network of electric charging points becomes more comprehensive and petrol stations become scarcer, the attractiveness of electric vehicles will rise.

“Just transition”

The state has a duty to make the transition to a green economy equitable by facilitating the shift to new jobs for workers affected by technological change (such as people employed in the coal, oil and gas sectors, those working in energy-intensive industries that are reliant on fossil fuels, such as the steel, cement and petrochemical sectors, and people living in communities where livelihoods are supported by large employers operating in fossil fuel-linked sectors). At the same time, governments also need to regulate jobs in the green economy from an environmental point of view and a health and safety perspective. In other words, the transition to a green economy needs to be just (see Box 4.5).

The extent of an economy’s vulnerability depends on a variety of factors, which vary substantially across the EBRD regions. They include the economy’s endowments in terms of fossil fuels, its industrial structures, workers’ skill-sets and the degree of labour market mobility. Importantly, the vulnerability of specific groups of workers is also driven by broad factors such as the competitiveness and location of industries within the economy.31

Around 40 per cent of the economies in the EBRD regions have a level of carbon intensity which is above the global average. Given the prevalence of fossil fuel subsidies across the EBRD regions (see Chart 4.11), consideration needs to be given to the distributional consequences of their removal in order to support those who are least able to afford higher energy prices. Importantly, NDCs have so far paid insufficient attention to the issue of economic inclusion. Only 25 per cent of all NDCs submitted by economies in the EBRD regions include plans for skills training, while many countries foresee no activities at all in relation to human capital.

The state is a major owner of fossil fuel assets in the EBRD regions, as discussed in Chapter 2. That is especially true of the coal sector, which employs more than 1.1 million people, both directly and indirectly, and is particularly vulnerable to any transition to a green economy in the short term. The public sector also has a crucial role to play in supporting the development of new economic opportunities in communities impacted by such a transition process. For example, the state may need to strengthen social safety nets and provide targeted support to displaced workers, including assistance with the acquisition of new skills linked to the needs of local labour markets, help finding new high-quality jobs, mental health support and financial counselling. In the EU, subnational regions that are highly reliant on carbon-intensive industries can be awarded EU funds to help support a just transition process, but they must first draw up a strategic plan detailing the measures that they plan to implement.32

When it comes to the removal of fossil fuel subsidies, a successful policy design will include measures aimed at increasing public support for reforms, adequate social protection for low-income households, the gradual phasing-out of the subsidies in question, and the establishment of adequate mechanisms to stop rapid price rises.33

Chart 4.13

Source: European Patent Office (PATSTAT database, spring 2020) and authors’ calculations.

Note: These data are based on patents filed with the European Patent Office in the period 1990-2019. “Advanced economies” exclude EBRD countries of operations that the IMF classifies as advanced economies.

Private-sector initiatives

Previous sections focused on the role of the state in the transition to a green economy. Ultimately, that role involves guiding private initiative in a sustainable direction, with the private sector responding to the incentives that it faces. This next section looks at the ways in which private firms can support that transition process.

Voluntary emissions targets

Against the backdrop of pressure from investors, and anticipating government policies that could penalise carbon emissions in the future, a growing number of companies have announced their own voluntary emissions targets (albeit the emissions covered still account for only a small fraction of the total emissions generated by human activities). Ikea, for example, plans to reduce its emissions by 15 per cent by 2030, including indirect emissions related to raw materials and consumers’ use of products. Apple, meanwhile, is committed to being 100 per cent carbon-neutral in terms of its supply chain and products by 2050.34 And BP, an oil and gas company, recently declared its intention to become a net-zero company by 2050.35

While these initiatives are welcome, there is little consensus on what “carbon neutrality” or “net-zero emissions” really mean, and there is no clear standard for calculating a company’s carbon footprint. Increasingly, however, companies are including emissions derived from their supply chains and emissions resulting from customers’ use of their products, in addition to their own emissions (such as those produced by their office buildings or company-owned vehicles).36

The Science Based Targets initiative (SBTi) seeks to fill that gap by establishing and promoting best practices in the area of evidence-based target setting, providing resources and guidance to help reduce barriers to the adoption and independent verification of companies’ targets.37 As of August 2020, a total of 433 companies have approved science-based targets, while a further 521 companies are committed to submitting their targets for validation within 24 months of signing up to the initiative.38 The majority of them (including both state-owned utilities and privately owned companies, most of which are listed) signed up to the initiative in 2019. Sixteen of those companies are located in the EBRD regions. What is more, one of the 16, Magyar Telecom in Hungary, has an approved target.

Companies in the EBRD regions are, on average, less prepared for the transition to a low-carbon economy than companies elsewhere. This is also reflected in assessments by the Transition Pathway Initiative (TPI), which looks at the quality of companies’ management of their GHG emissions and risks and opportunities relating to the transition to a low-carbon economy, as well as the current and targeted emissions intensity of each company in the context of international targets and national pledges made under the Paris Agreement.

Green labelling and certification

Increasingly – either voluntarily or as a result of regulation – firms in the EBRD regions are becoming more transparent about the environmental footprint of their products, including packaging, input materials, the energy that is consumed during production and the applicable environmental and health and safety standards. One option for firms that are looking to do this is to use an independently verified green-labelling scheme based on life-cycle considerations.

The European Commission has been working to simplify and improve green labelling and packaging. The EU Ecolabel, which was established in 1992, covers a wide range of different product groups, from manufactured goods to tourist accommodation. As of March 2020, more than 70,000 products have been awarded the EU Ecolabel in 24 different product categories. Of that total, 7,770 labels have been awarded in the EBRD regions – most of them in Greece (3,523), Poland (2,727) and Estonia (781). Other international schemes include Fair Trade, Green Seal, the Forest Stewardship Council, Excellence in Design for Greater Efficiencies (EDGE), Performance Excellence in Electricity Renewal (PEER) and Leadership in Energy and Environmental Design (LEED).

In addition, some countries have established their own national green-labelling schemes – which are, in turn, recognised by the Global Ecolabelling Network (GEN). National schemes in the EBRD regions include Eco-Labelling (run by Kazakhstan’s International Academy of Ecology), Vitality Leaf (run by Russia’s Ecological Union) and the Ecolabelling Programme (run by Ukrainian NGO Living Planet).

The role of international organisations

The evidence discussed above suggests that there is plenty of room for improvement in terms of companies’ readiness for the transition to a low-carbon economy in the EBRD regions. International organisations (including the EBRD) have a key role to play in supporting that transition, both as investors and as providers of capacity-building programmes.

One example of such support is an EBRD initiative, launched in 2018, which seeks to develop guidelines on enhancing companies’ governance in respect of climate-related risks and opportunities in emerging markets and helps firms to implement the required measures.39 The Corporate Climate Governance Toolkit enables companies to ascertain whether climate-related considerations are adequately integrated into their decision-making processes, as well as identifying ways in which that integration could be enhanced. Such initiatives can be supported by broader capacity-building programmes helping companies and governments to develop effective climate strategies and report on them. UNCTAD, for instance, has been advising managers of ports on climate risks and their mitigation.

The transition to a green economy can also be taken into account when prioritising investment, as is the case with the EBRD’s revised Green Economy Transition (GET) approach (termed “GET 2.1”). In addition to the specific attention that is paid to the issue of “just transition”, all investments are, by 2025, to be screened for alignment with the Paris Agreement and national climate-related action plans, with increased investment in projects focusing on the “greening” of the financial sector and energy systems, industrial decarbonisation, sustainable cities, food supply chains, the preservation of natural capital, opportunities relating to the circular economy and green digital solutions.

Conclusion

The transition to sustainable growth and a green economy will only be a success if the private sector applies its ingenuity, investment and entrepreneurship to that endeavour. However, a strong state – encompassing sound public policy, strong state institutions and determined political leadership – is needed to channel private-sector dynamism in the right direction. That does not mean central planning; it means that the state should incentivise companies and consumers to think green, promote clean investment and remove barriers preventing a smooth transition to the low-carbon economy of the future.

National governments – both in the EBRD regions and elsewhere – have yet to live up to their responsibilities in this regard. At present, the NDCs of economies in the EBRD regions under the Paris Agreement imply a further increase in GHG emissions over the next 10 years. Thus far, green laws and policies have only reduced GHG emissions by around 12 per cent relative to the levels that would otherwise be expected. Under the Paris Agreement, countries are expected to review and ratchet up their NDCs in the course of 2020. They must take this opportunity to radically increase their ambitions and align them with the Paris Agreement’s objective of restricting global warming to well below 2°C relative to average pre-industrial temperatures.

If they are to achieve that objective, countries must, in the short term, build the transition to a green economy into their Covid-19 recovery plans. Many of the government investment projects that are needed for the transition to a green economy (such as investment in clean energy and energy efficiency) are also effective ways of supporting the post-Covid-19 recovery.

The state must also be ruthless in focusing its support on industries and firms that have a zero-carbon future, while refraining from propping up zombie firms that will struggle in the green economy. Earmarking a percentage of those support packages for energy efficiency improvements, for example, could help firms that are currently underperforming to move closer to the energy efficiency frontier. The analysis in this chapter has found considerable heterogeneity in firms’ energy efficiency performance, which suggests that there is ample scope for such measures.

In the medium term, the state needs to address the market and policy failures that are impeding the transition to a green economy. The key here is to get prices right. That means putting a higher price on carbon and applying that higher price to a broader set of emission sources. It also means removing fossil fuel subsidies, which still total more than 1 per cent of GDP in the EBRD regions.

Additional incentives, subsidies and regulation are also needed to encourage greater resource efficiency, leverage network effects (for instance, ensuring that electric cars have access to a comprehensive network of charging points) and ensure access to capital for firms with viable green investment projects. Low-carbon solutions such as renewable energy and electric cars often entail significant capital costs at the outset (although their eventual operating costs may be low), which highlights the essential role that a well-functioning financial market plays in supporting the transition to a green economy.

In the longer term, the state must support the creative destruction that the transition to a green economy will unleash. Clean innovation has the same benefits as IT or nanotechnology in terms of knowledge creation. The fact that the wider societal benefits of green innovation far exceed the private returns to innovating firms justifies the provision of additional government support. At the same time, active policies aimed at seizing the opportunities presented by the transition to a green economy will need to guard against the common pitfalls of industrial policy, including capture by politically connected interests.

Because carbon-intensive economic activity is so deeply entrenched in the EBRD regions, the state will also have a key role to play when it comes to supporting workers and communities that are adversely affected by such creative destruction. The state has a duty to make that transition process equitable – for instance, by supporting labour market mobility and reskilling, and by enforcing labour standards to ensure the attractiveness of jobs in the green economy.

Box 4.1. The Covid-19 pandemic and attitudes towards climate change

Covid-19 and climate change share a few similarities: neither observes national borders; and in both cases, the worst damage can only be averted if society commits to decisive action in the face of a seemingly abstract threat.40 Indeed, the Covid-19 pandemic shows the size of the challenge that we face as regards climate change. Because of this, it has been suggested that the pandemic may increase awareness of climate change, with deliberative engagement mechanisms (such as citizens’ assemblies and juries) being a powerful way of building a social mandate for climate action post-Covid-19.41 At the same time, research carried out prior to the pandemic found that older generations (who face greater health risks as a result of Covid 19) were less likely than younger generations to regard climate change as a serious threat.42

This box investigates the relationship between age, the economic impact of the Covid-19 crisis and attitudes to climate change using individual-level data from a survey carried out in 2020 by the EBRD and the ifo Institute, which covered nearly 18,000 individuals in Belarus, Egypt, Greece, Hungary, Poland, Serbia, Turkey and Ukraine. Regression analysis is used to explain attitudes to climate change on the basis of various individual-level characteristics, such as age, gender, education, income decile, political views (left or right) and country of residence, as well as interaction terms combining a person’s age group (29-38, 39-48, 49-58 or 59-69, with 18-28 being the reference category) with a variable indicating whether an individual has been personally affected by the Covid-19 crisis.

The analysis shows that older respondents in those eight countries who have been economically affected by Covid-19 are significantly more likely to believe that global climate change poses a serious threat to them and their families than individuals of a similar age who have not been affected by the crisis (see Chart 4.1.1). For younger age groups, the corresponding differences are smaller. This finding is important, as older people make up a growing percentage of the voting public and affect the transition to a green economy through behavioural choices.43 Perhaps surprisingly, additional analysis (not reported here) reveals that this pattern is absent in six western European countries. This could be because the Chernobyl nuclear accident in 1986 has had a long-lasting impact on environmental awareness in parts of the EBRD regions, or it could be due to the fact that older generations in the EBRD regions grew up in a worse environmental situation as a result of the high levels of industrial pollution under central planning.

Taken together, the results of this analysis suggest that the Covid-19 pandemic could boost awareness of environmental issues and increase popular support for measures to address climate change, particularly in the EBRD regions.

Chart 4.1.1

Source: EBRD-ifo Institute survey and authors’ calculations.

Note: These estimates are based on linear probability models which regress an indicator of the perception that climate change is a serious threat on various individual-level characteristics, country dummies, and interaction terms combining age group dummies with a dummy variable indicating that a respondent has been economically affected by Covid-19. Coefficients for those interaction terms are shown in the chart. The 95 per cent confidence intervals shown are based on robust standard errors clustered at country level.

Box 4.2. Leveraging IT to facilitate the diffusion of green technology

It is often difficult for homeowners and businesses to identify the best-performing green technologies and the green financing programmes that will provide funding for such purchases. One way of addressing that challenge is through an online platform, such as the EBRD’s Green Technology Selector, which was launched in 2018. This online shopping-style platform acts as a global directory of best-in-class energy efficiency and renewable energy technologies, covering everything from solar panels and biomass boilers to thermal insulation.

The platform features products from all over the world, with technology vendors applying to have their high-end products included on the platform in order to make them more visible to prospective clients. Performance requirements for the technologies listed on the platform are periodically adjusted to reflect market developments.

Meanwhile, the EBRD’s new Tech Selector mobile app allows businesses and homeowners to explore more than 18,000 green technologies and identify those that are eligible for financing under special initiatives (such as the Green Economy Financing Facility,44 the Green Trade Facilitation Programme45 or the Finance and Technology Transfer Centre for Climate Change programme,46 all of which are run by the EBRD in partnership with local financial institutions). For instance, if a client decides to invest in green technology that is not available in their own country, they can benefit from a dedicated trade credit instrument provided by a financial institution participating in the EBRD’s Green Trade Facilitation Programme.

Box 4.3. “Greening” the financial system

Shifts in people’s awareness of the implications of climate change are beginning to influence the ways in which markets operate – with significant consequences for the global financial system. In particular, climate change considerations are being integrated into financial supervision and due diligence on prospective investments, including the assessment, management and disclosure of climate-related risks and opportunities by both financial and non-financial firms. Climate-related risks are broad in nature, encompassing both the potential for a decline in the profitability of carbon-intensive sectors and potential damage resulting from climate change. The most prominent market-driven initiative in this area is the Financial Stability Board’s Task Force on Climate-related Financial Disclosures (TCFD), which published recommendations in 2017 advocating voluntary climate-related financial disclosures for regulated financial and non-financial organisations.47

The Green New Deal and the Sustainable Finance Action Plan under the EU’s capital markets union are another example of an ambitious policy framework that seeks to steer the financial system towards climate-resilient sustainable development. Under those initiatives, the European Central Bank and Europe’s supervisory authorities are rolling out strategies aimed at integrating green disclosure requirements into their supervisory activities. Despite the existence of that common policy and supervisory framework, the fact that firms in central and south-eastern Europe are less familiar with disclosure practices poses particular challenges for the effective implementation of the framework across the EU. More broadly, there is a need to ensure that emerging market economies are able to adopt practices that support the greening of their financial systems.

The gap between those new supervisory expectations relating to the greening of the financial system and established market practices in the EBRD regions may require strategic intervention (even in economies outside the EU that are, to some extent, influenced by EU financial regulations). Such interventions may involve the provision of policy advice to policymakers, supervisors and financial firms, as well as targeted financial assistance for market participants.

At the same time, the limitations of using financial supervision as a means of promoting green industrial policies should be recognised. Central banks and financial supervisors are primarily responsible for ensuring financial stability. While responding to systemic climate-related risks to financial stability is entirely consistent with that mandate, most financial supervisors would not support the use of financial supervision to engineer the wider greening of the economy. The balance between greening the economy and prudential supervision of the financial system is a delicate one, with the two objectives not being fully aligned.

Box 4.4. Local content policies in the renewable energy sector

In addition to objectives relating to the green economy, governments also pursue a variety of other goals relating to employment and industrial and technological development, giving rise to complex choices. In this context, one group of policies that deserve particular attention are the local content provisions that are used in the renewable energy sector. The use of such policies in that sector increased in the aftermath of the 2008-09 global financial crisis, with such developments also being observed in some economies in the EBRD regions.48

When building infrastructure, producers of renewable energy can decide where to source their equipment from and on what terms. However, local content policies may encourage or require them to source a certain percentage of intermediate goods and services from local manufacturers or service providers. Such policies may involve a local content premium – a subsidy in exchange for the voluntary sourcing of domestic inputs – or a strict requirement whereby local content has to be at a certain level in order for a permit to be granted.

Governments often argue that such local content policies strengthen the national supply chain supporting the renewable energy sector. This is thought to be achieved in two ways: first, by boosting demand for goods produced by local manufacturers, who will then invest in expanding their activities, both in scale and in scope, thereby growing the local value chain; and second, because international equipment manufacturers or technology companies will be inclined to set up local manufacturing subsidiaries or develop supplier relationships with existing local companies, so as not to be constrained by local content requirements or to benefit from local content premia.

However, empirical evidence suggests that local content policies in the renewable energy sector are unlikely to reliably increase demand for locally produced equipment. Instead, they are likely to result in a number of risks and costs:49

- First, they increase production costs and end-user tariffs, driving energy prices up, or they require significant public spending on local content premia.

- Second, they result in distortions, with the creation of value chains and jobs simply coming at the expense of activity in other sectors.

- Third, local content policies do not have an established track record of helping to build sustainable, competitive and innovative value chains in the renewable energy sector, given that such policies do not help the sector to become competitive in the long run through long-term investment or innovation.

- And fourth, such policies contravene World Trade Organization (WTO) rules and other international trade agreements.

Evidence from case studies looking at local content policies in the Russian, Turkish and Ukrainian renewable energy sectors provides further support for these arguments. In Russia, multiple rounds of procurement were conducted between 2013 and 2019, with the required level of local content rising from 25 to 70 per cent. As of December 2019, only 56 per cent of the planned renewable energy capacity for the period 2014-19 has been commissioned. In Turkey, a number of tender procedures have been conducted since 2016, with conditions including a requirement that the successful tenderer establish manufacturing capacity in the country that is equivalent to 70 per cent of the equipment required. Thus far, however, none of the projects in question have reached the construction phase. And in Ukraine, local content premia were introduced in 2015 through higher feed-in tariffs for eligible projects, with only a modest impact to date.

In the above examples, local content policies do not seem to have played a significant role in the development of value chains in the renewable energy sector. Indeed, it could be argued that they have, instead, been associated with delays in the deployment of new renewable energy capacity, driven by unsuccessful auctions, a lack of uptake of local content premia and implementation delays. In 2020, the Kazakh government took note of the above evidence and decided to abandon its plans to incorporate local content premia in its tender procedures in the renewable energy sector.

There are other, less risky, non-distortionary policies that have had some success in triggering the development of local value chains and job creation.50 For instance, supplier development programmes aimed at establishing sustainable cooperation between local and international firms have the potential to foster innovation through the diffusion of technology.

Box 4.5. “Just transition” – making the green economy inclusive

The Paris Agreement of December 2015 commits parties to “taking into account the imperatives of a just transition of the workforce and the creation of decent work and quality jobs in accordance with nationally defined development priorities”.51

Numerous countries have pledged to ensure a “just transition”, signing up to initiatives such as the Solidarity and Just Transition Silesia Declaration adopted at the 2018 United Nations Climate Change Conference (COP 24) or the ILO’s Climate Action for Jobs Initiative, with dedicated approaches being developed both at country level and at regional level (as in the case of the EU’s Just Transition Mechanism, for instance).

The term “just transition” generally refers to measures that help workers to take advantage of opportunities to obtain new, higher-quality jobs linked to the green economy, while also protecting those who are at risk of losing their jobs. Such measures include labour market policies, skills training, social safety nets and action to support regional economic development. For example, the EBRD’s “just transition initiative” focuses on the reconversion of high-carbon assets, the rehabilitation of land, other green investment that fosters local employment and reskilling, and entrepreneurship support programmes for those affected by the transition to a green economy. Pilot initiatives are due to be run in cooperation with both national and regional authorities.

Annex 4.1. Comparing the ambition levels of NDCs

NDCs contain a variety of different mitigation targets and vary in terms of the years in which those objectives are to be achieved, the methodologies that are employed, and the base years against which those targets are measured (see Table A.4.1.1). Nevertheless, it is still possible to compare them, as this annex explains. In order to be able to compare the ambition levels of those various submissions, a common target year (2030) has been chosen, along with a common base year (2010). What is more, while the EU’s NDC sets an absolute target of a 40 per cent reduction in GHG emissions by 2030 relative to 1990 levels, the commitments specified in EU (2018) have been used instead, with 2005 as their base year, in order to better reflect the actual commitments of EU member states. Those targets exclude sectors participating in the EU Emissions Trading System, which have been tasked with reducing their emissions by 43 per cent between 2005 and 2030.

The first step involved estimating the targeted level of GHG emissions in 2030. For countries with an absolute target to be achieved by 2030, that estimate was based on the most recent NDC. For countries with a BAU target to be achieved in 2030, the implied level of emissions in 2030 was derived from the Pledge Pipeline produced by Jörgen Fenhann at the UNEP DTU Partnership.52 For countries with carbon-intensity targets relative to GDP, estimates of economic growth produced by the EBRD, the IMF and the OECD were used (assuming that the estimate for the last year available was applicable to all subsequent years). For countries with carbon-intensity targets relative to population, median variant population estimates derived from the UN’s 2019 Revision of World Population Prospects were used. Linear extrapolation was applied in the case of countries with a target year other than 2030.53

Second, a common base year of 2010 was applied. A recent base year helps to minimise the impact that idiosyncrasies in countries’ previous emission paths have on the comparison. Where 2010 levels of GHG emissions could not be obtained from NDCs, CAIT estimates were used.54

In order to assess how far countries have come in terms of meeting their NDC targets, progress between 2010 and 2016 (the most recent year for which comparable GHG emission data are available) was assessed to provide an indication of the further efforts that are needed to achieve the objectives set out in NDCs. While the comparisons provided are dependent on a large number of assumptions, they are a useful indication of the relative degree of ambition in the various NDC targets.

Annex 4.2. Assessing green laws and policies

The analysis in this chapter draws on two databases providing details of laws and policies relating to climate change and the environment.

First, the IEA Policies and Measures Database provides comprehensive details of a wide variety of green policies and laws. As of August 2020, it contains more than 5,600 laws and policies across 150 economies, going all the way back to the 1950s, and covers everything from local municipal measures to international endeavours. It also spans a wide range of subject areas, from waste management and infrastructure for electric vehicles to renewable energy subsidies and building standards, with policies and laws being classified by type, industry and subject area. The subject areas with the most measures are energy efficiency and renewable energy, while the industries with the most measures are electricity, heating and transport. The database records the year in which each measure is implemented, rather than the year of its adoption (as well as indicating the status of measures that have been discontinued or have not yet entered into force).

Second, the Climate Change Laws of the World database (which is run jointly by the Grantham Research Institute on Climate Change and the Environment at the London School of Economics and the Sabin Center for Climate Change Law at Columbia Law School) contains, as of August 2020, more than 1,900 national level and EU laws and policies relating to climate change, covering climate change mitigation and adaptation, as well as disaster risk management. It contains data on 197 economies – all UN member states and parties to the United Nations Framework Convention on Climate Change (UNFCCC), as well as non-members such as Kosovo and the West Bank and Gaza – with laws and policies dating as far back as 1947. It also distinguishes between acts passed by a legislative body and policies or measures decreed by an executive authority (such as the government or president). Around 60 per cent of all entries in the database are laws, and the remaining 40 per cent are policies. The database covers a wide range of sectors, including buildings, taxation and green finance, energy supply and demand, industry, transport and land use, and forestry conservation and management. However, it does not cover nuclear energy, gases that harm the ozone layer or general environmental laws. And, in contrast with the IEA database, it only includes measures that are still in force.

The analysis in this chapter draws on both databases. As the IEA database contains mostly policies, while the Climate Change Laws of the World data focus on laws, the two combine to provide a good overview of the international landscape of green laws and policies. Those data have, in turn, been further supplemented with information on laws and policies in Kosovo, North Macedonia and the West Bank and Gaza, which has been obtained from government websites and reports by international organisations.

This chapter only considers the 1,036 laws and 4,107 policies that were in force across the 197 economies in 2020. It first excludes the 59 EU laws and 68 EU policies, before using an alternative approach that assigns those laws and policies to all EU member states (which accounts for the possibility that the existence of EU laws and policies reduces the need to adopt measures at country level).

References

Acemoğlu, P. Aghion, L. Bursztyn and D. Hémous (2012)

“The environment and directed technical change”, American Economic Review, Vol. 102, No. 1, pp. 131-166.

P. Aghion, A. Dechezleprêtre, D. Hémous, R. Martin and J. Van Reenen (2016)

“Carbon taxes, path dependency, and directed technical change: Evidence from the auto industry”, Journal of Political Economy, Vol. 124, pp. 1-51.

H. Allcott and M. Greenstone (2012)

“Is there an energy efficiency gap?”, Journal of Economic Perspectives, Vol. 26, No. 1, pp. 3-28.

A. Bowen and S. Fankhauser (2011)

“The green growth narrative: Paradigm shift or just spin?”, Global Environmental Change, Vol. 21, pp. 1157-1159.

S. Carattini, M. Carvalho and S. Fankhauser (2018)

“Overcoming public resistance to carbon taxes”, WIREs Climate Change, Vol. 9, No. 5, e531.

CDP, World Resources Institute and WWF (2015)

Sectoral Decarbonization Approach (SDA): A method for setting corporate emission reduction targets in line with climate science.

D. Coady, I. Parry, N.-P. Le and B. Shang (2019)

“Global fossil fuel subsidies remain large: An update based on country-level estimates”, IMF Working Paper No. 19/89.

A. Dechezleprêtre, R. Martin and M. Mohnen (2017)

“Knowledge spillovers from clean and dirty technologies”, Grantham Research Institute on Climate Change and the Environment Working Paper No. 135.

A. Dechezleprêtre and M. Sato (2017)

“The impacts of environmental regulations on competitiveness”, Review of Environmental Economics and Policy, Vol. 11, pp. 183-206.

EBRD (2011)

Special Report on Climate Change: The Low Carbon Transition, London.

EBRD (2017)

Transition Report 2017-18 – Sustaining Growth, London.

EBRD (2019)

Transition Report 2019-20 – Better Governance, Better Economies, London.

EBRD (2020)

The EBRD just transition initiative: Sharing the benefits of a green economy transition and protecting vulnerable countries, regions and people from falling behind, London.

S.M.S.U. Eskander and S. Fankhauser (2020)

“Reduction in greenhouse gas emissions from national climate legislation”, Nature Climate Change, Vol. 10, No. 8, pp. 750-756.

EU (2018)

Regulation (EU) 2018/842 of the European Parliament and of the Council of 30 May 2018 on binding annual greenhouse gas emission reductions by Member States from 2021 to 2030 contributing to climate action to meet commitments under the Paris Agreement and amending Regulation (EU) No 525/2013.

H. Frumkin, L. Fried and R. Moody (2012)

“Aging, Climate Change, and Legacy Thinking”, American Journal of Public Health, Vol. 102, No. 8, pp. 1434-1438.

Y. Füllemann, V. Moreau, M. Vielle and F. Vuille (2020)

“Hire fast, fire slow: The employment benefits of energy transitions”, Economic Systems Research, Vol. 32, pp. 202-220.

Gallup (2018)

“Global Warming Age Gap: Younger Americans Most Worried”.

H. Garrett-Peltier (2017)

“Green versus brown: Comparing the employment impacts of energy efficiency, renewable energy, and fossil fuels using an input-output model”, Economic Modelling, Vol. 61, pp. 439-447.

K. Gillingham and K. Palmer (2014)

“Bridging the energy efficiency gap: Policy insights from economic theory and empirical evidence”, Review of Environmental Economics and Policy, Vol. 8, pp. 18-38.

U.E. Hansen, I. Nygaard, M. Morris and G. Robbins (2019)

“Local content requirements in auction schemes for renewable energy: Enabler of local industrial development in developing countries?”, UNEP DTU Partnership Working Paper Series 2017, Vol. 2.

V. Haralampieva (2019)

“Ramping up Climate Action by Enhancing Companies’ Governance Framework”, Law in Transition Journal, pp. 32-41.

C. Hepburn, B. O’Callaghan, N. Stern, J. Stiglitz and D. Zenghelis (2020a)

“Will Covid-19 fiscal recovery packages accelerate or retard progress on climate change?”, Oxford Review of Economic Policy, Vol. 36.

C. Hepburn, N. Stern and J. Stiglitz (2020b)

“Carbon pricing”, European Economic Review, Vol. 127.

High-Level Commission on Carbon Prices (2017)

Report of the High-Level Commission on Carbon Prices, Carbon Pricing Leadership Coalition.

L. Hook (2018)